With the onset of the COVID-19 pandemic, the financial world has witnessed a swelling wave of Buy Now Pay Later (BNPL) companies; a wave that started with the global crisis in early 2020 and one that is still rising today with an imminent crash shrouded in uncertainty.

Can trendy BNPL services lose traction in the near future? Let’s take an in-depth look into the short-term financial model to establish cause and context.

Surprisingly, BNPL is not a modern concept. The idea of buying goods now and paying for them later dates as far back as the 19th century, when sewing machine giant “Singer” sold their reputable machines on a “dollar down, dollar a week” model.

Today, BNPL is popular for different reasons, but the logic remains the same; consumers get the option to pay for their purchases in installments over an extended period of time, with no interest. To make that possible, BNPL companies impose a transaction fee on retailers, whether online or at defined points of sale, and consumers benefit from being able to split their payments over usually four installments.

In the post-pandemic age of digital dominance, online transactions are largely still preferred to brick-and-mortar, which means more and more consumers are seeking alternative solutions to debt-based credit card systems.

After all, credit cards have by and large been the same since the 1950s, a fact that presents a clear conflict with the high-tech nature of the financial scene as we know it today. Add to that the global financial crisis of 2008 and reckless interest rates, and the credit card system is just begging for a worthy alternative.

This is where BNPL comes in. The BNPL model is a “twofer” for buyers and sellers in that it allows customers who are short on cash to break down big purchases into smaller payments, while at the same time increasing traffic to merchants, opening up their industry to a segment with significantly larger spending power.

BNPL services approvals are easier to come by compared to lines of credit and credit cards, and are also usually free of interest at different points of sale, making them a stronger alternative to high-interest credit cards with a high annual percentage rate (APR).

BNPL in the U.S & Europe

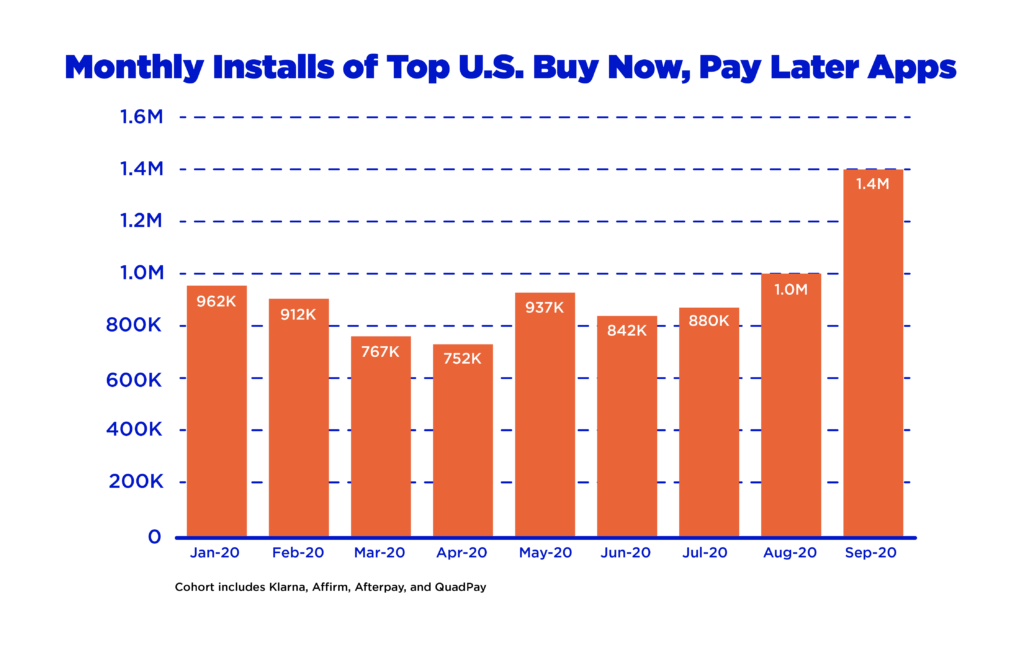

Taking a look at the popularity of BNPL during 2020, the peak of the COVID-19 pandemic in the U.S. corresponds to a rise in BNPL app downloads, with a noticeable 1.4M spike in September 2020 downloads, as per a survey conducted by SensorTower.

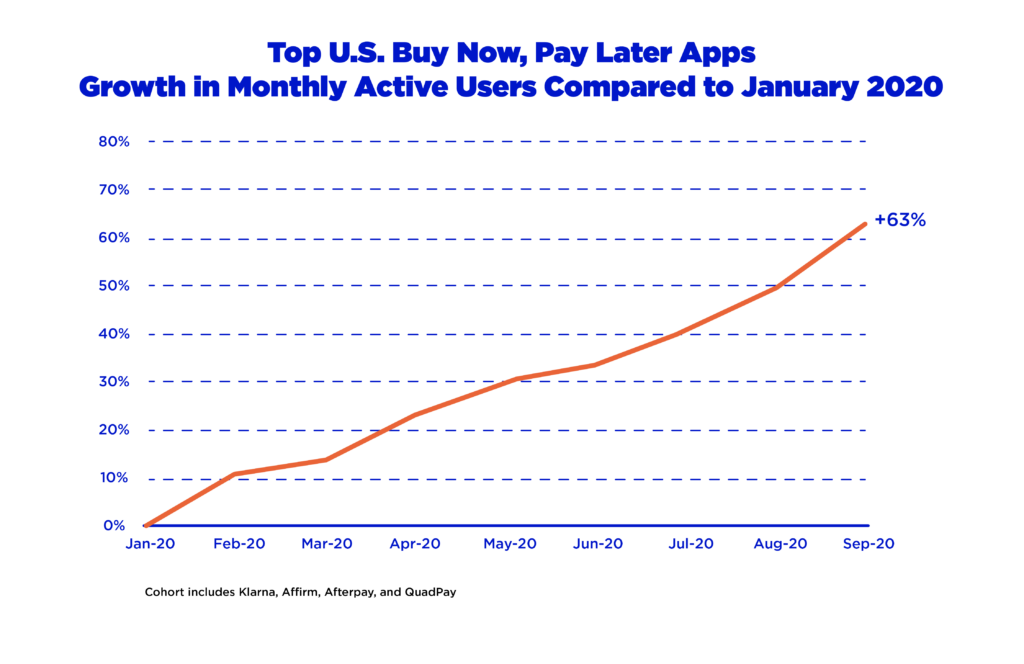

During that same month, BNPL apps operating in the U.S. also witnessed a 63% increase in MAUs (Monthly Active Users) when compared to January 2020.

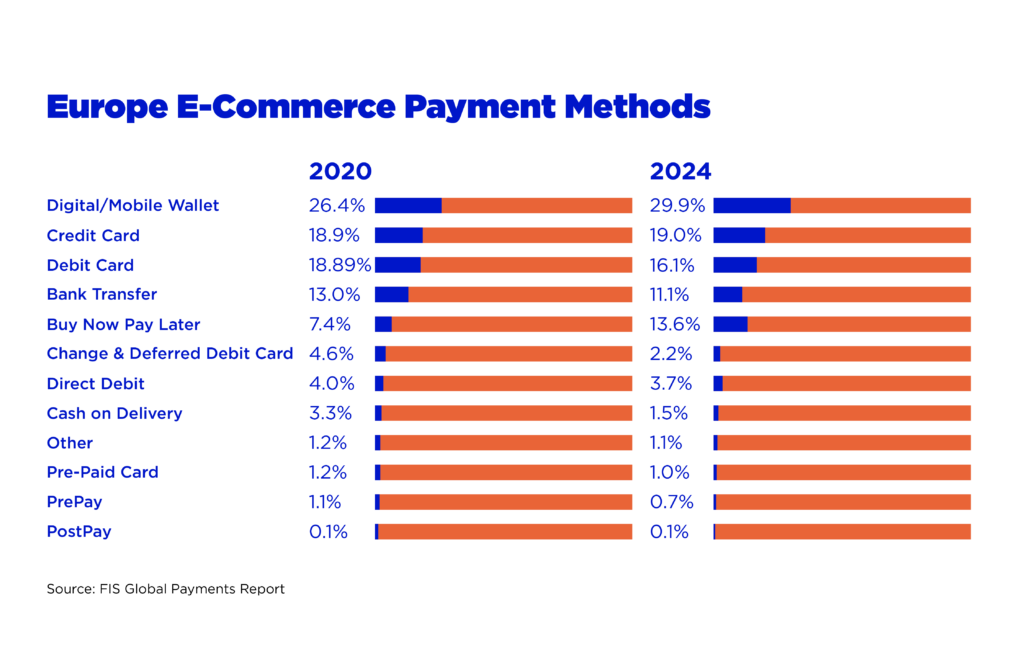

In Europe and the U.K., the 2020 FIS Global Payment Report results predict that BNPL use in Europe and the United Kingdom will almost double by 2024 (13.6%) when compared to 2020 (7.4%).

This brings us to the impact of COVID-19 on BNPL in 2021. Between March and April 2021, C+R Research surveyed 2,005 online consumers in the United States, where 51% of respondents were male and 49% were female. The results lend a compelling perspective on just how much the COVID-19 pandemic contributed to the rise of BNPL.

According to GlobalData, BNPL transactions accounted for $2 in every $100 spent in e-commerce in 2021.

As consumers began to spend more time and money online, the scope of Buy Now, Pay Later applications widened to accommodate the looming uncertainty of the global economic status quo. Unemployment, market shortages, dwindling cash reserves and many more factors meant that people of all age groups were affected by economic hardships and purchase indecision.

The many benefits of BNPL, like periodic installments and interest-free repayments, offered the perfect short-term solution to a long-term problem.

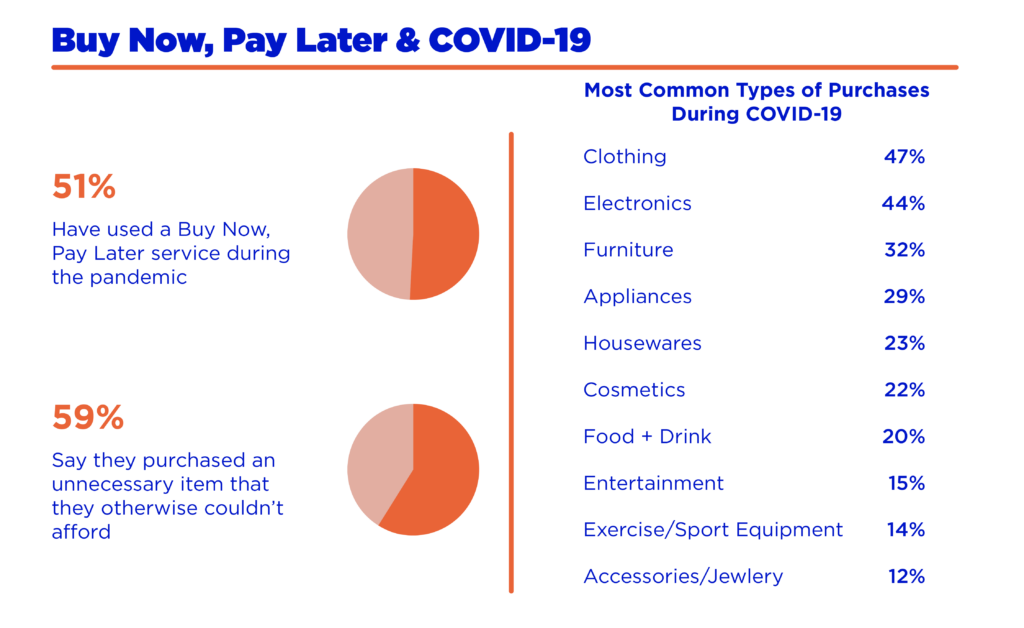

51% of the surveyed respondents said they used BNPL services during the COVID-19 pandemic, especially for clothing (47%), electronics (44%), and furniture (32%).

Although these products do not qualify as basic “needs”, people took to online shopping to fend off the impact of the pandemic on their lives, finding relief and consolation in buying more stuff.

And indeed, of the surveyed consumers who shopped using BNPL, 59% said they bought an unnecessary item that they could not afford before, making BNPL a double-edged sword that came to their aid at times of economic instability, but one that could also end up wounding them in the long-term.

By the end of 2021, COVID-19 had started to slow down, which led to the resurgence of offline shopping. BNPL companies soon realized that brick-and-mortar businesses also represent the fertile ground.

As such, they started partnering up with leading merchants and offline retailers to integrate BNPL financing at cashiers and checkouts, building integrated shopping experiences, and rewarding BNPL customers with exclusive offers and programs to further engage and reel them in, inside or outside their homes.

Today, BNPL is alive and well among most Gen Z-ers, Millennials, and even tech-savvy Gen X-ers. Yes, even some 55+ year-olds are now enjoying the advantages of BNPL as apps become more intuitive, user-friendly, and easier to use.

BNPL in the Middle East

Following the rise of digital payment adoption between the years 2020 and 2021, the last year alone saw a significant spike in the amount of new and existing players that have started offering BNPL services. Boasting more than ten established players in the region, many of whom are already funded or on their way to be, the MENA region is fertile ground for a budding BNPL ecosystem that fosters financial inclusion, improving purchasing power across all demographics.

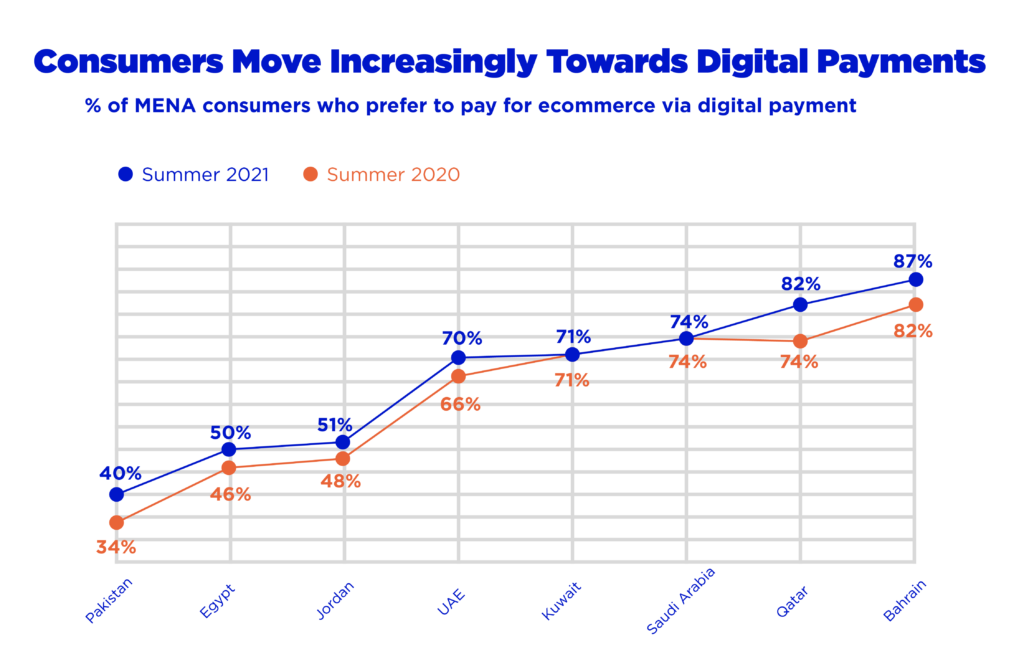

Compared to 2020, 2021 marked a shift in preferences when it comes to using digital payment methods in the MENA region, with Bahrain coming in the first place as 87% of its population preferred digital payment, an 5% increase from the previous year. Qatar follows suit at 82% (an 8% increase) and Saudi Arabia at 74%.

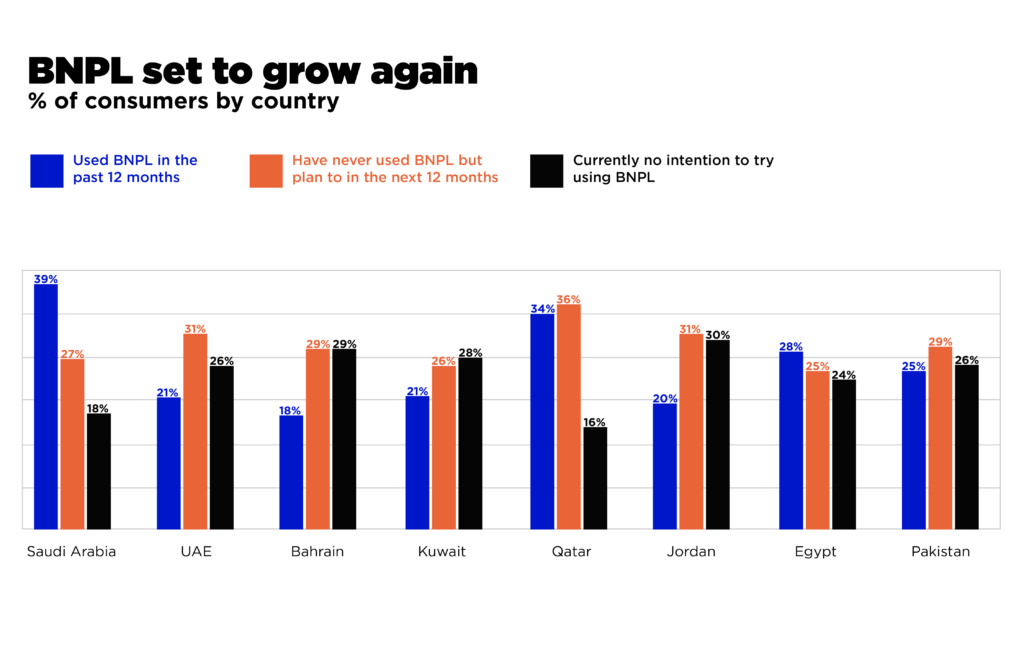

In order to get a better understanding of just how popular BNPL is becoming in the MENA region, let’s take a look at the results of a survey of more than 13,000 respondents conducted by payment solution provider Checkout.com (2021) in the MENAP region (To fit the scope of this article, Pakistan will be excluded from the results).

The 2021 survey shows Saudi Arabia spearheading the pack with 39% of participants stating that they used BNPL applications during the past year.

Qatar comes in second at 34%, followed by Egypt at 28%, a remarkable achievement for Egypt in particular, whose population is roughly triple that of Saudi Arabia and Qatar put together, and a great indicator that BNPL is here to stay.

Although the UAE, Jordan, and Bahrain were all below the 22% mark in terms of BNPL usage over the last year, respondents of these three countries said they plan to use BNPL next year.

Top BNPL Players in the MENA region

Looking at the GCC region, we find many leading BNPL players that are poised to potentially expand their operations in the region and beyond, such as Tamara in Saudi Arabia, Tabby, Payby, Cashew, Postpay, and Spotii in the UAE, as well as Taly in Bahrain.

It’s worth noting that the most prominent BNPL players in the GCC region in terms of funds raised are Tabby ($32 million), Tamara ($6 million), Postpay ($5.5 million), and Spotii ($1 million).

As for the rest of the African continent, the most established BNPL companies include Payflex in South Africa in which Australian BNPL firm Zip bought a 25% stake in 2021, as well as Lipa Later in Kenya and Credpal in Nigeria.

BNPL in Egypt

The past few years have witnessed a thriving Egyptian Fintech ecosystem, largely due to the ongoing digital transformation happening on a national level, one that is empowered by the Central Bank of Egypt, public & private financial institutions, investors, stakeholders, and a prospering startup ecosystem.

As was the case with the rest of the world, COVID-19 presented a great opportunity for growth and maturity in the country.

For BNPL, the projected annual growth of payments in Egypt is at 132%, and BNPL payment adoption is expected to reach $434.7 million in 2022.

Although Egypt might not yet have an abundance of BNPL players when compared to the general Fintech arena, existing BNPL companies are thriving.

The key players in the BNPL ecosystem in terms of market share today include Fawry (one of Egypt’s very first FinTech entities), Shahry (who has recently raised $0.65 million), Valeo, and most notably; EFG Hermes’ valU.

When EFG Hermes Holding launched valU as a subsidiary in 2017, BNPL payments were still in their infancy. The term was not even coined at the time. Today, valU has become the leading Buy Now Pay Later lifestyle-enabling FinTech platform in the MENA region.

In July 2022, valU announced a partnership with Amazon Egypt introducing BNPL, providing Egyptians with flexible, affordable, and convenient payment options when shopping on Amazon.

Walid Hassouna, CEO of valU, said “We are happy to expand our collaboration with Amazon to deliver on our mission to provide all customers with unrivaled access to products and services over convenient payment plans. valU allows customers the flexibility to make purchases without having to deplete their cash reserves and makes it easier for them to accommodate unplanned but needed purchases into their budget. By taking advantage of deferred payment methods, customers have more freedom to spend without the fear of feeling squeezed financially.”

In August 2022, valU announced that it had acquired 100% of Paynas, a digital HR and payroll management system that allows employees to receive their salaries upfront, among other solutions that focus on employee management and benefits. The acquisition boosted both sides. Where valU got access to Paynas’ client list of micro, small, and medium enterprises (MSMEs), Paynas had access to valU’s BNPL facilities. This visionary collaboration opened up more opportunities for consumers to engage with BNPL services, and MSMEs also benefited from this partnership.

Now that we have the bigger picture, we can ask the big question: Is it all smooth sailing for Buy Now, Pay Later models? Is BNPL really the much-anticipated alternative to credit?

If you had asked almost anyone in 2020, the answer would have probably been a resounding yes, because at the time, it only had good things to offer in light of the mid-pandemic global state of affairs.

In 2022, however, consumers who have used BNPL in the last few years are starting to feel the repercussions of buying goods at one time and needing to pay for them at another.

Let’s explore some of the challenges faced by BNPL customers in the short and long run, their implications, and why BNPL might not be the best choice when it comes to replacing traditional credit as we know it.

In March 2022, UK-based independent organization Citizens Advice carried out a survey of 2,288 people who used BNPL services in the last 12 months.

Although 42% of respondents mentioned that they took to borrowing in more than one way in order to pay their due installments, credit cards were by far the most popular option. More than half (51%) of 18 to 34-year-olds also needed to borrow money to repay their pending BNPL payments

In addition to credit cards, the respondents borrowed from friends and family, and took personal loans, payday loans, and overdrafts to be able to continue paying their BNPL commitments.

The added increasing inspection of regulators could also make things tougher for service providers.

Moreover, one or more of these factors encouraged people to cut back on spending on non-essential goods and services; a stark distinction from how people used BNPL at the peak of the COVID-19 pandemic.

It is also worth mentioning that although one of the biggest appeals of BNPL is that it is hardly dependent on an individual’s credit score, this advantage does not necessarily apply to all BNPL firms.

Some companies have taken to conducting a hard credit score check when people apply to their BNPL services, but it should also be noted that some of the leading players in the BNPL arena, such as Klarna, Affirm, Afterpay, and PayPal, do soft or even no credit checks before allowing individuals to access BNPL services.

So does that mean BNPL usage affect or does not affect your credit score?

Typically no, but this answer is given on the assumption that you are not late in paying your due installments.

BNPL firms are known to impose late fees on consumers who are late to continue their payments or fail to do so, and prolonged payment delays or failure to pay off one’s due amounts could increase the chances of your credit score is negatively affected.

However, this worrisome side of BNPL is not enough to thwart consumers so far. Apple announced earlier this year at the 2022 WDC keynote address in June that it is launching its first BNPL product, Apple Pay Later, which will be complementary to Apple Pay and native to iOS 16, Apple’s upcoming operating system for iPhone.

The key takeout from this new player is that millions of retailers in the U.S., Europe, and the rest of the world already accept Apple Pay, which grants Apple Pay Later an inherited distribution network with millions of users who are perfectly poised to start using this service right away.

Like its popular counterparts, the new service will enable consumers to pay for their purchases in four installments over six weeks, will be free of interest, and will also require a soft credit check, as well as a review of Apple customers’ transaction history.

JP Morgan Chase has also recently deployed a BNPL solution that allows consumers to pay for their purchases over many months with no interest at a small monthly fee.

So does that mean that BNPL is still a viable payment model?

Well, it depends on which market leaders you ask. Sweden-based Klarna, one of the top BNPL companies that were valued at $46 billion after a funding round last year, lately had to lay off around 10% of its workforce.

With so many BNPL entities competing for market dominance around the world, one question raises: since BNPL companies more or less provide the same core service, what exactly sets these players apart from each other?

At this point in time, the distribution might be the single best answer here. BNPL players are in constant competition to secure the highest number of quality merchants in the least possible time in an attempt to secure a vast network of payment facilitators, thus increasing the availability of BNPL for customers around the world. Companies that reach the most viable merchants first have a competitive advantage. After that, it’s up to them to retain and expand their network.

So what is the final verdict? Is BNPL a great alternative to credit in general during these fast-paced times, or is it a long-term debt trap that people of all ages are falling into?

When it comes to consumers, mass adoption rates indicate a strong desire to engage with BNPL models, and whether delaying payments to a more convenient date entails stronger purchasing power and better economic stability, or if it just delays the inevitable accumulation of debt is yet to be determined in the long run.

But although the benefits are obvious, the drawbacks, are not so much. Where BNPL could be considered a viable short-term financing solution, it’s the long-term handling of delayed installments that can be considered the ultimate deciding factor.

Here’s one last question to think about:

What happens when you convince an entire generation to spend more than it can realistically afford?

Only time can tell.

If you see something out of place or would like to contribute to this story, check out our Ethics and Policy section.