How central banks set interest rates, manage liquidity and control exchange rates, what we call monetary policy, deeply impacts capital flows, credit availability, and investment strategies.

The MENA region is at an economic crossroads, striving to contain inflation without crushing growth. This tightrope walk is underpinned by diverse regional monetary policies, which are, in turn, fundamentally reshaping capital flows, bond yields, and investor approaches, opening doors to both risks and exceptional opportunities.

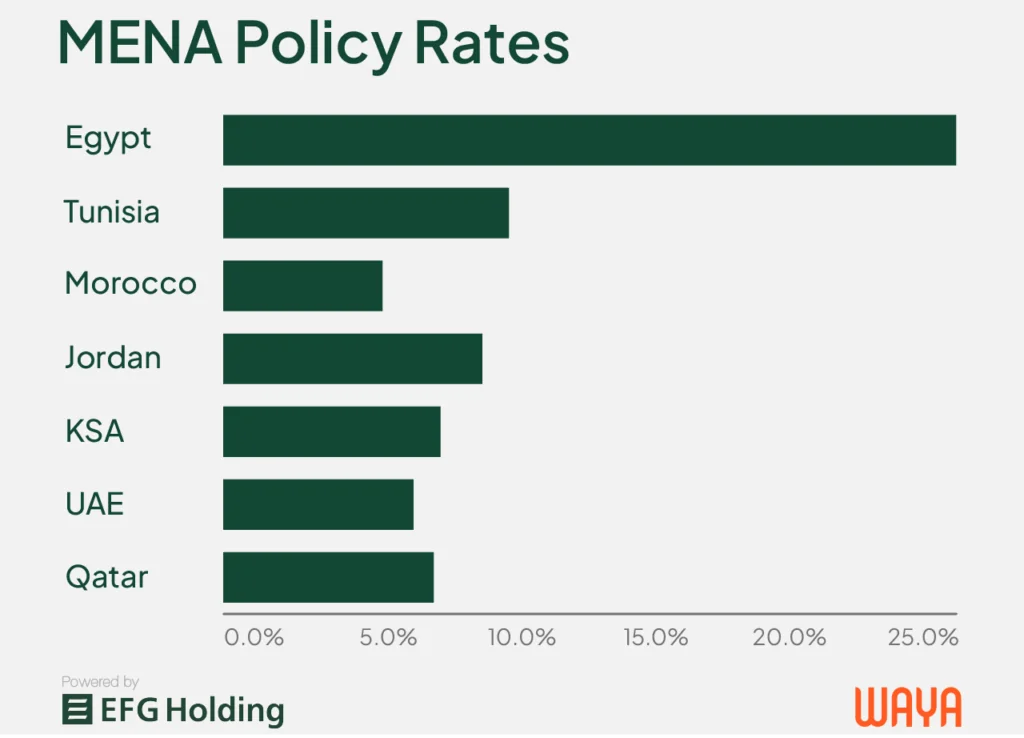

A Tale of Two Monetary Models

When looking at the MENA region for economic power, our gaze naturally turns to the oil-rich powerhouses of the GCC. Their currencies are pegged to the U.S. dollar, meaning their monetary policies echo those of the U.S. Federal Reserve. Rate hikes are imported, but deep reserves and sovereign wealth funds soften the impact.

But shift your focus to the reform-driven corners of MENA: Egypt, Tunisia, and Morocco, and a different scenario emerges. These countries rely on flexible exchange rates to manage global shocks, granting them greater control, but also exposing them to inflation shocks, FX volatility, and investor flight.

Monetary decisions in these economies, be it raising interest rates or adjusting the currency, have widespread effects on debt markets and how investors move their money.

By the Numbers: Policy Echoes in Markets

Each country’s interest rate stance is not just a macroeconomic choice; it actively signals its intentions and stability to financial markets:

- In 2024, both Egypt and Tunisia made it much more expensive to borrow money, tightening monetary policy.

But by mid-2025, their economic strategies began shifting:

Egypt started easing, cutting its policy rate to 24.00% from a high of 27.25%.

Tunisia, on the other hand, maintained its interest rate at 8.00% through early 2025 before a slight reduction to 7.50% in May.

- Morocco and Jordan pursued a gentler approach, raising rates only as needed to curb inflation without stifling economic growth.

- GCC nations, bound by their currency pegs, found their monetary tools limited. However, their abundant wealth funds provided enviable resilience.

What’s Driving Investor Behavior?

One major trend is the carry trade, a strategy where investors borrow money in countries with low interest rates and invest it in countries with high interest rates to earn the difference, or “carry”.

- Carry trade capital is flooding into Egypt, lured by yields above 25% post-currency float and IMF reforms.

- But not all high-yield stories are equal: Tunisia offers high rates too, but limited investor confidence (due to low CCC+ credit ratings and restricted market access) keeps inflows muted.

Another trend is Sukuk, which are Islamic financial instruments similar to bonds, but structured to comply with Islamic law (Shariah), which prohibits interest. Green sukuk is a recent development, funding eco-friendly projects and providing ethical, interest-free returns.

- Green Sukuk and ESG bonds are emerging as policy-aligned tools to attract long-term capital. For instance, the $1.5 billion green sukuk from UAE’s DP World was oversubscribed twofold, underscoring robust demand for top-tier Islamic debt instruments.

A “flight to quality”is evident among investors. May 2025 saw the bulk of investment flow into top-tier banks like Al Rajhi and Mashreq, as well as sovereigns including Bahrain and Oman.

Strategic Shifts: Unlocking New Opportunities

As monetary policy continues to shape financial conditions across MENA, investors and corporates alike are recalibrating their strategies. The interplay between interest rates, inflation, and capital access is giving rise to new patterns in fixed income, Islamic finance, and equity markets.

1. Fixed Income Frontiers

Egypt is now one of the most attractive carry trade destinations. Why? A rare combination of high yields (25%+) and easing inflation post-currency float.

Meanwhile, Morocco and Jordan offer sovereign yields in the comfortable 5–6% range with far less volatility, making them ideal for the more conservative fixed-income investor.

2. Sukuk’s Resilience

Islamic finance is staging a robust comeback. In May 2025 alone, sukuk issuances surged to $15.6 billion, demonstrating renewed momentum and growing investor interest.

What’s particularly exciting is the emerging potential in green sukuk, a promising new frontier. This area is getting a significant boost from initiatives like the Saudi Green Initiative, which seamlessly blends environmental goals with Sharia-compliant investment principles.

3. Banking Sector Strength

Leading the charge are UAE banks, with strong net interest margins (NIMs) at 3.4%. Saudi and Qatari banks are also seeing robust performance, successfully utilizing Fed rate pass-throughs to boost their profitability.

4. Equity Value Plays

Egyptian exporters in areas such as fertilizers, agribusiness, and logistics are benefiting FX depreciation tailwinds, making them attractive investments. Why?

When the Egyptian pound weakens, Egyptian products become more affordable and competitive on the global market. This is a big win for export-focused companies because they earn revenue in strong foreign currencies (like USD or EUR) while paying many of their costs, such as local labor or rent, in the weaker local currency.

In Saudi Arabia, the equity story is different, but still tied to monetary policy. Due to its dollar peg, the Saudi Arabian Monetary Authority (SAMA) largely aligns its interest rate decisions with the U.S. Federal Reserve. When the Fed increased rates, SAMA did too, which pushed up lending rates for Saudi banks. Crucially, deposit rates didn’t rise as much, expanding the banks’ net interest margins (NIMs).

The result?

Saudi banks are now earning more money from lending activities while maintaining relatively low funding costs. Bank stock prices haven’t fully reflected their increase in profitability, meaning many remain undervalued despite their strong performance. They also maintain strong return on equity (ROE), which measures how efficiently banks are using shareholder capital to generate profits.

Stakeholders’ Guide to Building Stability

For Investors:

- Short-term: For those seeking higher yields, Egypt’s T-bills and GCC corporate sukuk currently offer compelling returns.

- Medium-term: Increase exposure to Saudi and UAE bank equities and ESG-linked infrastructure projects.

- Long-term: As inflation begins to ease across the region, particularly in high-volatility economies like Egypt and Tunisia, there’s a growing possibility that MENA monetary policies will gradually converge. This alignment could usher in more predictable financial conditions. By positioning themselves now, whether through undervalued equity markets or favorable bond yields, they could achieve significant long-term gains

For Corporates

- Secure financing through sukuk or bonds now, before anticipated Fed rate cuts reverse current yield advantages.

- Actively hedge currency risk in markets with flexible regimes, such as Egypt and Tunisia.

If you see something out of place or would like to contribute to this story, check out our Ethics and Policy section.