By the Numbers is a biweekly data-driven series in partnership with EFG Holding that unpacks business news and economic trends across the MENA region. Through visuals and statistics, each edition brings clarity to the numbers shaping the future of our region.

Embedded finance is quietly reshaping how people borrow, save, and spend across MENA.

It’s Already Happening—And You’ve Probably Used It

You’re at checkout, buying groceries online. Instead of reaching for your card, you choose to pay in installments in the app, thanks to Valu. Or maybe you were browsing for a used car and got offered a loan before you even spoke to a bank.

This isn’t a glimpse into the future. It’s already here. Finance has moved from standalone bank apps into the platforms you use every day. No extra logins. No paperwork. Just a few taps and you’re approved.

What Is Embedded Finance?

Embedded finance refers to financial products like loans, insurance, or savings that are built directly into non-financial platforms. That means services like Buy Now Pay Later (BNPL), micro-loans, and wallets can now be accessed inside your ride-hailing app, e-commerce checkout, or even food delivery platform.

It’s a shift away from banking as a destination and toward banking as a seamless, invisible part of your digital life. Instead of opening a bank app, finance shows up exactly when—and where—you need it.

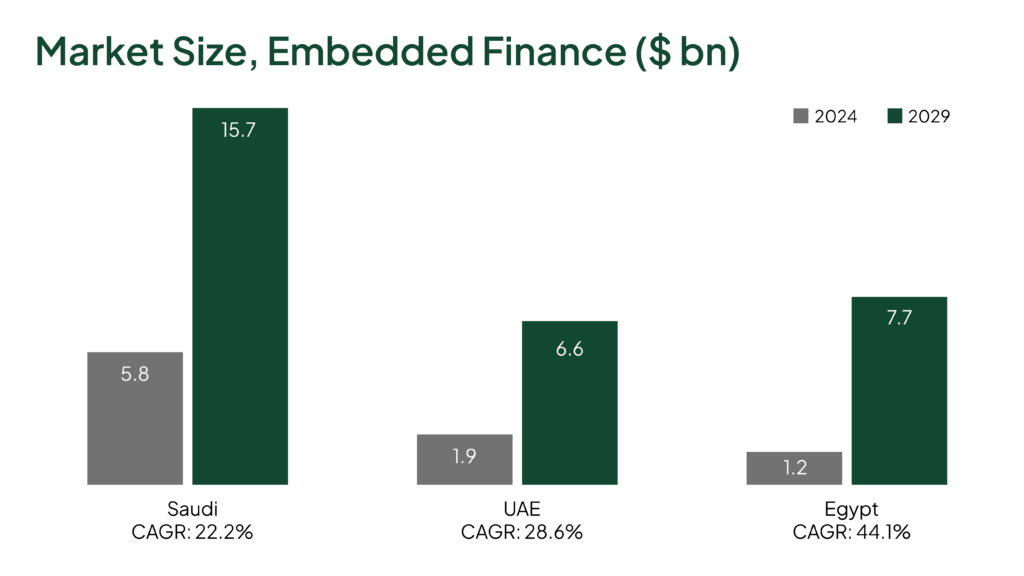

By the Numbers: The MENA Growth Story You Can’t Ignore

Data tells the story best. Across MENA, embedded finance is growing at breakneck speed:

- Saudi Arabia leads the region in market size: $5.8B in 2024, projected to hit $15.7B by 2029.

- Egypt shows the fastest growth, with a 44.1% CAGR over the same period.

- Africa and the Middle East’s share of the global embedded finance market is expected to rise from 9.6% in 2024 to 15% in 2029, growing at nearly double the global average.

This growth is part of a broader fintech boom. McKinsey forecasts that MENA will be the fastest-growing fintech region globally, with net revenue rising 35% annually through 2028, more than double the global pace.

A key driver? Demographics. A quarter of the region’s population is under 30, and in Saudi Arabia, Egypt, and the UAE, that figure is over 50%. These digital-native consumers are eager for financial services that live inside their favorite apps.

But how is this growth translating to real-life tools?

How Embedded Finance is Rewriting the Rules (And Your Daily Life)

From AI-powered credit to ride-hailing wallets, embedded finance is reshaping how people interact with money. Here’s what’s happening:

AI, as Usual

Platforms are using AI to personalize offers and manage risk, adjusting BNPL terms or flagging fraud based on your behavior.

Behind the scenes, fintechs feed these systems with alternative data, like e-commerce activity and telco usage, to underwrite loans for people with little or no credit history.

For users, that means tailored tools. For fintechs, smarter lending decisions.

Startups Lead the Way

MENA’s fintech ecosystem is thriving. The sector’s funding grew at 39% CAGR from 2020 to 2024, surpassing $1B annually in 2022 and 2023.

One result? The rise of super-apps: platforms that combine payments, savings, lending, and even insurance, all in one place.

Banks Are Jumping In

Legacy players aren’t standing still.

In 2024, 41% of banks had adopted embedded finance solutions, and nearly half expanded banking-as-a-service offerings.

Instead of competing, banks and fintechs are increasingly collaborating, merging trust, scale, and tech under one roof.

The Challenges Under the Surface: Risks, Gaps, and Exclusion

Despite the momentum, embedded finance in MENA still faces serious barriers:

Fragmented Regulation

There’s been some progress. In 2025, regulators across MENA are shifting from policy to execution. Saudi Arabia already has a full open-banking framework, while the UAE and Bahrain have launched sandboxes. Egypt is expected to follow soon.

Still, scaling across the region remains tough. Each country has its own licenses, data laws, and clearing systems. A single fintech expanding across the Gulf might spend six months just on local compliance.

Cross-border payments remain a headache too: slow, expensive, and fragmented. Without greater regulatory alignment, region-wide embedded finance will continue to face friction.

Financial Exclusion

While financial inclusion in the UAE has reached 94% as of May 2025 (according to a recent Daleel survey), many parts of the region still lag far behind. In non-wealthy MENA countries, only 48% of adults have bank accounts—23 percentage points below the developing-country average—limiting who can fully benefit from embedded finance in the first place.

Still, embedded finance is being leveraged to bridge this gap. Take Valu’s recent partnership with Vezeeta and Geidea: By integrating flexible payment plans into Vezeeta’s healthcare platform, Egyptians without private insurance can now access surgeries and lab tests through installment plans. This isn’t just convenience; it’s a lifeline for millions to prioritize their health without financial collapse.

Risk & Trust

Without financial literacy, users can slip into overindebtedness. At the same time, many in the region still distrust non-bank finance, so embedded finance requires a new level of trust and strong safeguards. Cybersecurity, data privacy, and user protection aren’t just nice to have; they’re essential to wider adoption.

How to Make the Most Out of This

If you’re a user:

Read the terms before taking a loan. Use platforms regulated by your country’s central bank. And treat in-app financing like any other form of credit: it’s real money you’ll have to repay.

If you’re a startup:

Strategic partnerships can unlock serious scale. Banks offer capital and compliance muscle; fintechs bring the tech. From white-label cards to co-branded loans, MENA’s most successful players are teaming up, not competing. And according to McKinsey, many are now turning to AI to improve efficiency, personalize offers, and boost profitability.

Just don’t cut corners on trust. Transparent design, Arabic UX, clear fees, and strong security signals like ISO certifications or sandbox approvals all help build credibility. To avoid debt risks, consider offering safeguards like spending alerts or optional credit limit caps.

A New Era of Finance, Without the Bank App

At this point, you surely know that embedded finance is already a part of your life. It isn’t just about speed or scale, it’s about changing habits. As more people borrow, pay, and save within the apps they already use, the line between tech and finance is fading fast.

For MENA startups, regulators, and everyday users, this moment is a turning point: a chance to make financial access more useful, more intuitive, and more inclusive.

If you see something out of place or would like to contribute to this story, check out our Ethics and Policy section.