Egypt is at a crossroads in its economic journey as it faces growing IMF pressure. As it grapples with inflation, mounting foreign debt, and uncertain growth, the nation’s relationship with international financial institutions, particularly the International Monetary Fund (IMF), is under scrutiny.

President Abdel Fattah El-Sisi recently hinted at a potential reevaluation of the IMF agreement, drawing attention to the challenges Egypt faces.

To gain insight into the challenges, it’s helpful to compare Egypt’s economy with Argentina’s 2001 and Lebanon’s 2019 crisis. This article examines the similarities between these situations and discusses how Egypt’s current circumstances may align with or differ from these historical events.

Egypt’s USD 3B IMF Deal: A Double-Edged Sword

The current agreement between Egypt and the International Monetary Fund (IMF) is centered on a USD 3B Extended Fund Facility (EFF) that was signed in December 2022. This agreement aims to stabilize Egypt’s economy by addressing its structural weaknesses, particularly focusing on fiscal consolidation, reducing debt, and ensuring exchange rate flexibility. Today, Egypt’s economy faces growing IMF pressure as it attempts to meet the signed agreement.

As part of the deal, Egypt committed to cutting subsidies, implementing tax reforms, and boosting exports. The IMF program was structured to restore investor confidence and secure Egypt’s foreign reserves, but these measures have contributed to rising inflation and increased costs of living for everyday Egyptians.

The government is now rethinking the deal, with President El-Sisi suggesting that Egypt might need to reassess its obligations to ensure the agreement aligns better with the country’s long-term economic goals and social needs.

A Fragile Economy Under IMF Pressure?

Egypt’s current economic predicament bears similarities to Argentina’s 2001 crisis and Lebanon’s 2019 meltdown. Both countries were burdened by high foreign debt, inflation, and dependency on external financial support. Egypt faces a similar situation today.

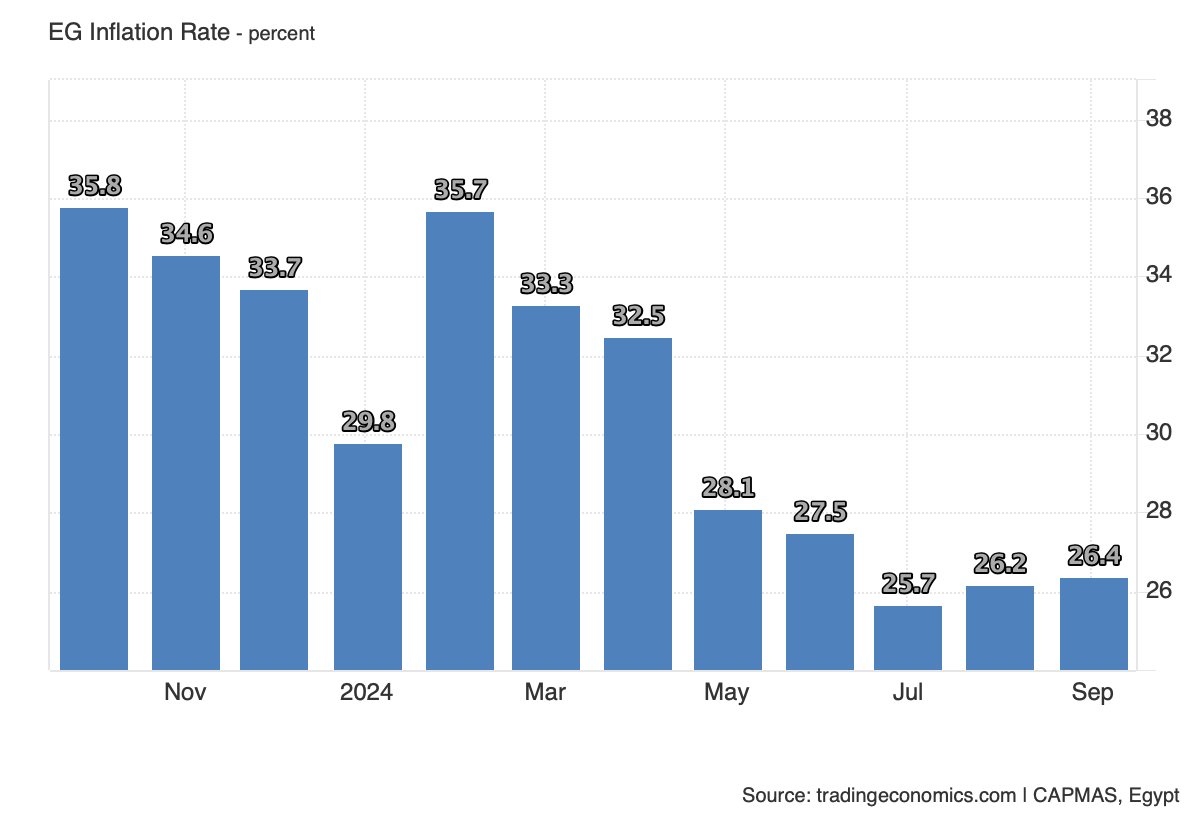

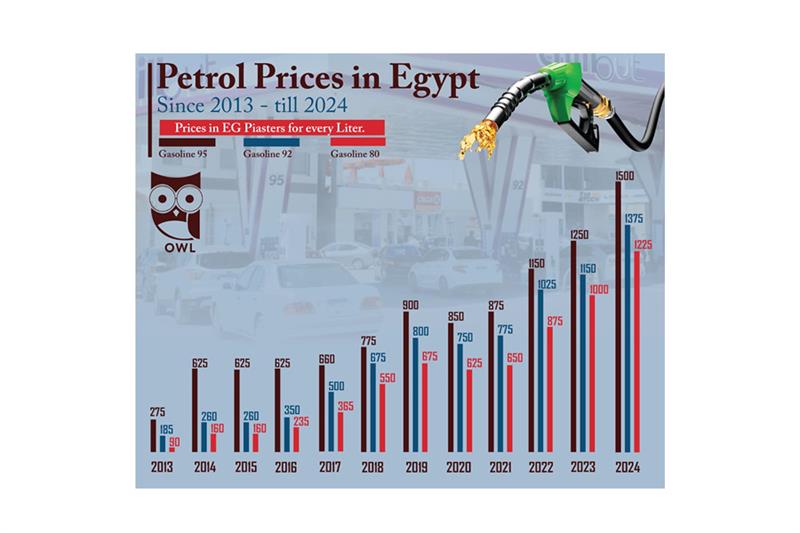

With inflation rates hovering around 30% in 2024, the country struggles to manage both internal and external pressures. The recent hikes in fuel prices have further worsened living standards for many Egyptians, while foreign debt obligations put immense pressure on the government’s budget.

President El-Sisi recently stated that Egypt must “reassess the situation with the IMF,” expressing frustration with the economic situation under the IMF’s program. Like Argentina, which entered a series of agreements with the IMF before its 2001 collapse, Egypt has relied on international financial support to stabilize its economy.

However, both cases illustrate that IMF-led solutions, while beneficial in some aspects, can lead to severe social consequences when coupled with austerity measures. Inflation, which heavily affects low- and middle-income Egyptians, mirrors the struggles faced by Argentina’s population, where high inflation controlled with IMF-imposed austerity measures caused social unrest.

Furthermore, Lebanon’s crisis was exacerbated by reliance on foreign borrowing and an overvalued currency, contributing to the country’s financial collapse. Egypt, while not in a full-blown financial crisis, faces similar risks if inflation and foreign debt continues unchecked.

The World Bank recently lowered its growth forecast for Egypt to 2.5%, citing inflation and external debt as significant obstacles. Lebanon, which had one of the highest debt-to-GDP ratios globally, serves as a cautionary tale for Egypt, which has seen its foreign debt balloon to nearly USD 165B in recent years.

Balancing IMF Commitments and Domestic Needs

Egypt’s relationship with the IMF has been central to its economic management. The USD 3B Extended Fund Facility (EFF) agreed upon in December 2022 was designed to stabilize Egypt’s economy by addressing structural weaknesses. However, the cost of adhering to IMF conditions has been felt most acutely by Egypt’s population.

The government’s recent hike in fuel prices, in response to IMF-imposed subsidies cuts, reflects the balancing act Egypt must perform between meeting its IMF obligations and addressing domestic discontent.

While the IMF’s program aims to promote fiscal stability, there is a growing debate over whether such measures align with Egypt’s long-term economic goals.

Argentina faced similar dilemmas during its economic collapse. IMF policies, while designed to stabilize Argentina’s economy, contributed to massive protests and political unrest due to the harsh austerity measures. Argentina’s economy eventually defaulted, causing severe long-term consequences.

Lebanon’s government also implemented IMF-inspired policies but failed to carry out meaningful reforms, leading to hyperinflation, a banking collapse, and widespread protests.

In Egypt, the public’s dissatisfaction with rising prices and stagnant wages does not mirror the unrest seen in Lebanon and Argentina. For the same, the Egyptian government deployed a battery of economic policies to effectively manage the economy.

In response to growing concerns, for example, Egypt’s central bank has issued EGP 50 billion in treasury bills to manage short-term liquidity needs. While this provides temporary relief, it does not address the underlying issues of inflation and debt.

Another policy adopted by the Egyptian government is currency devaluation. Egypt’s currency lost considerable value against the US dollar, creating further challenges for an economy that imports much of its food and energy.

Potential Paths to IMF Pressure Reduction

Egypt has options to mitigate its economic crisis, though none are easy. First, reevaluating its agreement with the IMF could allow Egypt to pursue more flexible financial policies.

Argentina renegotiated its terms with the IMF after its 2001 collapse, and while it took years for the economy to stabilize, the country eventually found a more sustainable path. Lebanon, on the other hand, failed to negotiate effectively with international creditors, leading to a drawn-out crisis that the country has yet to fully recover from.

Second, Egypt could focus on structural reforms that promote sustainable growth. Reducing reliance on debt and improving domestic production, particularly in agriculture and energy, could alleviate some of the pressure on foreign reserves. The recent hike in fuel prices, while unpopular, could encourage energy efficiency and reduce the country’s import bill.

However, without corresponding measures to increase wages or create jobs, such reforms may only deepen social discontent.

Egypt’s decision to potentially reevaluate its relationship with the IMF may also signal a desire to assert more control over its economic policies. Argentina’s and Lebanon’s failure to reform in time, combined with its heavy reliance on external borrowing, serves as a stark warning.

If you see something out of place or would like to contribute to this story, check out our Ethics and Policy section.